TCC's ESG Highlight: First Disclosure of sustainability/ climate-related financial information

- Home

- Sustainable E-newsletter

- TCC's ESG Highlight: First Disclosure of sustainability/ climate-related financial information

Governance 2024 Vol.02

TCC's ESG Highlight: First Disclosure of sustainability/ climate-related financial information

- #Sustainability-related Financial Disclosure

-

Tony Cheng|Research, Office of Responsibility and Sustainability

In June 2023, the International Sustainability Standards Board (ISSB) announced the IFRS S1/S2 standards, making the financialization of sustainability information a global trend. In August of the same year, the Financial Supervisory Commission immediately announced that enterprises with a capital of NT$10 billion will need to disclose related information according to S1/S2 by 2026, aiming to enhance the international climate financial information transparency of Taiwanese enterprises and strengthen the prevention of greenwashing, contributing to Taiwan's effort towards a net-zero transformation by 2050.

Chairman Nelson Chang of TCC Group Holdings tasked the Office of Responsibility and Sustainability and the Finance Department to form a cross-departmental team, launching a six-month trial project on S1/ S2. From researching standards and disclosure topics to how to integrate and link accounting items, in the absence of any precedent to follow and without any disclosure examples from the government and the IFRS Foundation, TCC completed its first Sustainability and Climate-related Financial Information Disclosure Report in April 2024. This also provides a new framework for reviewing TCC's internal operational model and investment strategy, promoting financial performance and long-term value creation.

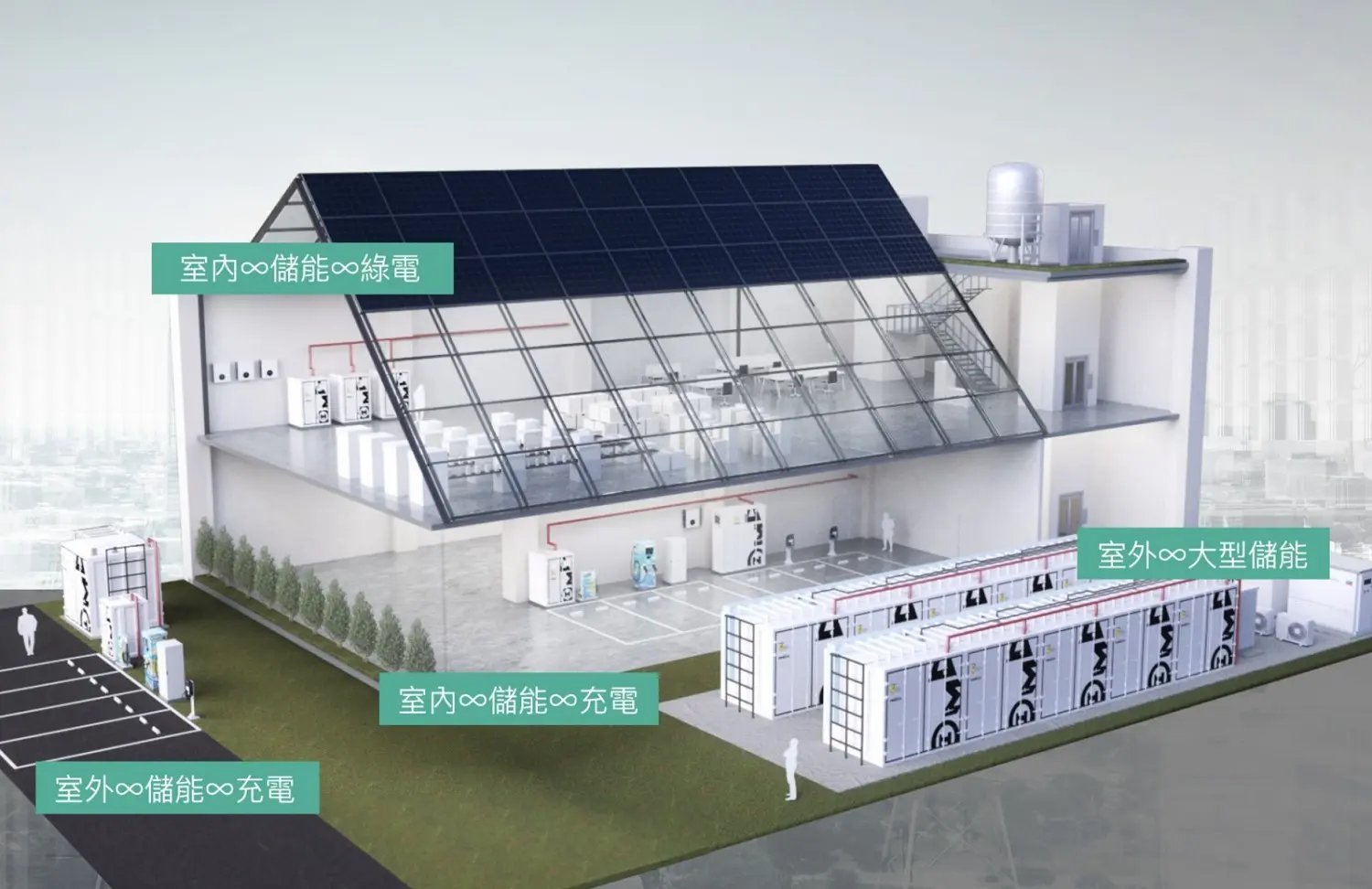

From the perspective of the primary users of general-purpose financial reports, including current and potential investors, lending banks, and other creditors, the project team based on the results of the 2023 double materiality analysis and strategic development focus, identified three material sustainability topics: "Climate Action and Net Zero Emissions," "Green Energy and Storage," and "Sustainable Products and Services." These topics identify reasonably expected sustainability and climate-related risks and opportunities that will impact TCC's outlook, and are a long-term commitment to sustainable development from TCC. Meanwhile proving that efficient operations through the disclosure of transparent financial figures under these three themes.

Let's quickly review the highlights of TCC's 2023 sustainability financial performance

THE SUMMARY OF TCC'S 2023 SUSTAINABILITY FINANCIAL PERFORMANCE | ||

DIVERSITY | Carbon reduction and green investment capital expenditure accounts for 68% of the total capital expenditure: TCC Group Holdings, spanning across Europe, Asia, and Africa, has invested in low-carbon construction materials, fully laying out the new energy industry chain, thereby diversifying its revenue streams. In the fiscal year 2023, the capital expenditure allocated to carbon reduction and green initiatives amounted to NT$16.875 billion, accounting for 68% of the total capital expenditure of NT$24,726 billion. |

|

RESILIENCE | 100% funded with operations generated cashflows: In 2023, TCC's total capital expenditure accounted for less than 80% of the net cash inflow from operating activities. In the fiscal year 2023, the net cash inflow from operating activities amounted to NT$33.75 billion, which is sufficient to fully cover the investment for low-carbon and new energy transition in the same year, while maintaining a robust balance sheet and cash flow statement.

| |

GROWTH | Profit attributable to the parent company grew by 48%: Continuing to invest and maintain positive profitability, the net profit for the year 2023 reached NT$10,005 billion, of which the net profit attributable to the parent company reached NT$7.998 billion, representing a net profit growth of over 140% compared to the year 2022, and net profit attributable to the parent company increased by approximately 48%. |

|

2023 FINANCIAL IMPACT

Unit: in Thousands NTD | Climate Actions and Net-Zero Emissions | Green Energy and Energy Storage | Sustainable Products and Services | Total |

Revenues | 748,807 | 5,817,397 | 39,279,069 | 45,845,273 |

Revenues (Onyx Ta-Ho Environmental Services Co., Ltd. Included) | 3,788,519 | 5,817,397 | 39,279,069 | 48,884,985 |

Cash Inflow from EU Subsidy | - | 371,713 | - | 371,713 |

Capital Expenditures | 5,218,254 | 11,539,175 | 117,523 | 16,874,952 |

Net Cash Inflow from Operating Activities | 33,751,150 | 33,751,150 | ||

Sustainable and Green Financing Cash Inflow | 30,829,871 | 30,829,871 | ||

Three Features to Understand TCC's Sustainability Financial Performance Disclosure Aligned with IFRS S1/S2

Feature 1. Quick grasping TCC's capital utilization of business transformation

One of the challenges enterprises face in sustainability information disclosure has always been the diverse needs of stakeholders, spanning environmental, social, and governance issues, making the disclosed information not necessarily helpful for investors' decisions. TCC's IFRS S1/S2 chapter information is comprehensive, allowing investors to quickly understand the result of TCC's three core businesses, key points of capital utilization, and sources of funds, even only by cross-referencing the "Sustainability Financial Performance Summary" (above table) with TCC's consolidated financial report.

Feature 2. Identifying results of Material Sustainability Topics with Double Materiality

TCC conducts material sustainability topics identification every two years. TCC adopt double materiality approach to analyzing the impact of a company's activities this year, benchmarking against the latest European Union Sustainable Development Reporting Standards (ESRS) trends.

Selecting topics with a high impact on corporate value (financial aspect) as disclosure items based on double materiality analysis is a significant breakthrough, as there are no clear regulation on materiality thresholds in the current IFRS S1/S2 articles. Through double materialit analysis, TCC focuses on three significant topics, which are high-impact items determine by executive management for the corporate value.

Feature 3. Enhanced comparability and verifiability of information quality

According to the IFRS Effects Analysis report in June 2023, the Environmental Resources Management Sustainable Development Institute (ERM) conducted a survey in 2022 among American institutional investors and companies, estimating that large institutions or investors spend an average of nearly $1 million annually on collecting and analyzing climate-related data for their investment decisions. Therefore, the introduction of IFRS S1/S2 is crucial for investors and financial institutions. As this is the first year of disclosure for TCC, it is expected that related financial data will be disclosed in the same manner in the future, allowing investors to concretely analyze TCC's revenue performance and proportion in transformation investment, the return on capital invested in low-carbon development, or the carbon reduction effect per dollar.

AUTHOR

Tony Cheng|A practitioner with a finance and sustainability backbone

With a background in finance and banking, an internship opened the door to sustainability work. After graduation, he immediately engaged in sustainability work, having worked in sustainability consulting firms and social enterprises. Gradually moving from a young sustainability worker to middle age, he firmly believes that we don’t inherit earth from our ancestors; we borrow it from our children.

-

Latest News 2024 Vol.02 Four Pillars of Revenue: Taiwan Cement Corporation Announces Transform into TCC Group Holdings

Latest News 2024 Vol.02 Four Pillars of Revenue: Taiwan Cement Corporation Announces Transform into TCC Group Holdings -

Environmental 2024 Vol.02 Want to reduce carbon emissions? Want sustainability? You can't do without BESS virtual power plants

Environmental 2024 Vol.02 Want to reduce carbon emissions? Want sustainability? You can't do without BESS virtual power plants -

Environmental 2024 Vol.02 TCC Production Plant's Small Revolution for Energy Saving and Carbon Reduction

Environmental 2024 Vol.02 TCC Production Plant's Small Revolution for Energy Saving and Carbon Reduction -

Social 2024 Vol.02 DAKA Ecotourism Guide explore the delicious tastes of tribal communities after earthquake

Social 2024 Vol.02 DAKA Ecotourism Guide explore the delicious tastes of tribal communities after earthquake -

Environmental 2024 Vol.02 The Avoid Emissions of TCC's Low-Carbon Products and Services

Environmental 2024 Vol.02 The Avoid Emissions of TCC's Low-Carbon Products and Services

TCC GROUP HOLDINGS

SUSTAINABLE E-NEWSLETTER.